Poland’ s games industry has undergone a transformation over the past two decades from a ‘marginalised success story’ to a globally recognised innovation hub, which today ranks alongside powerhouses such as Finland, Japan and the United States.

Games developed on the Vistula have become a key element of the country’s international soft power, promoting its culture and technological proficiency around the world.

The foundations of this success lie in the unique historical circumstances – the political transition, the accession to the EU which attracted investment, and the early dominance of personal computers which forced the development of deep technical competence.

Scale of success: a decade of exponential growth

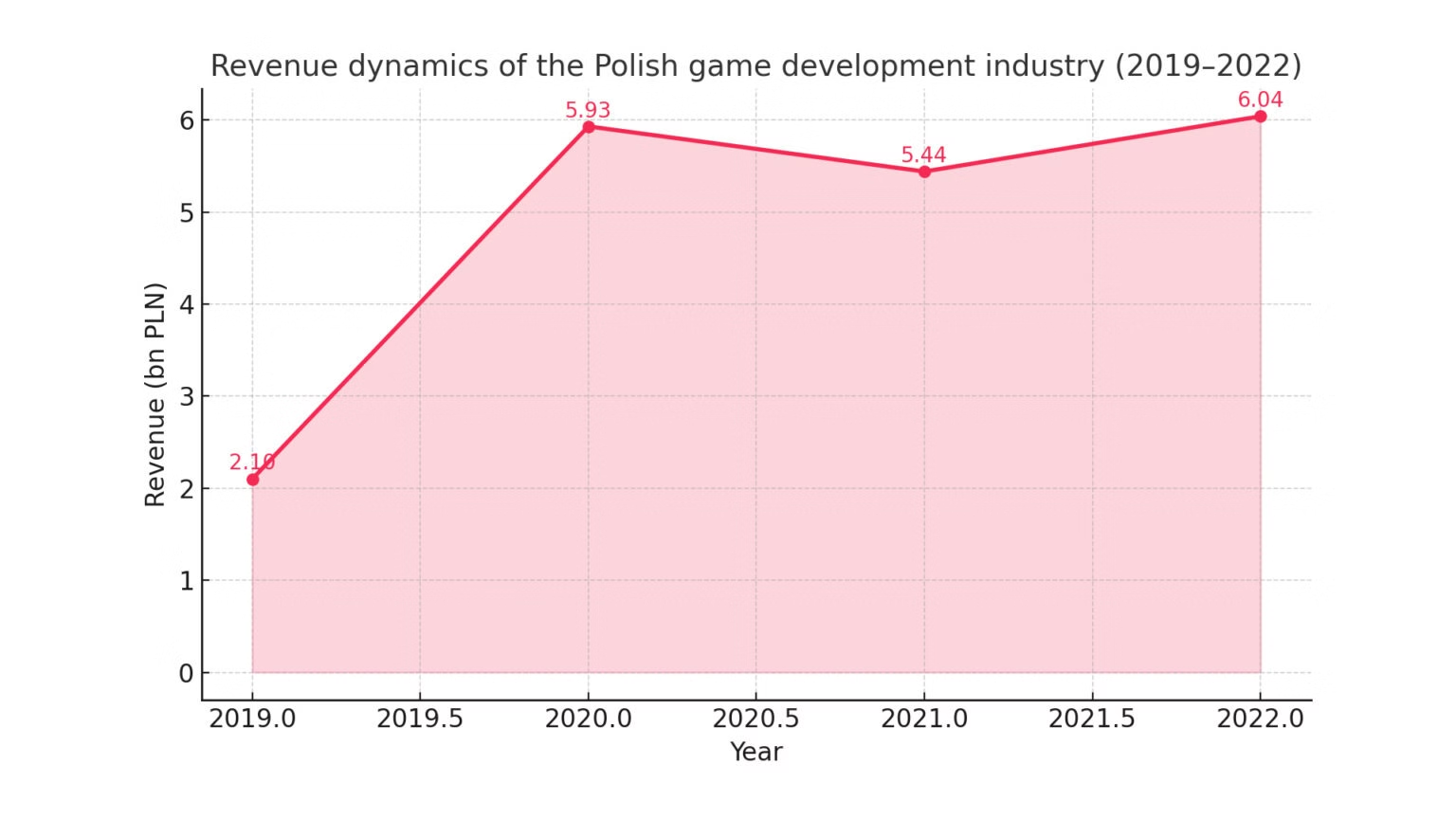

The figures best illustrate the dynamics of Polish gamedev. In 2022, the industry generated revenues of €1.286 billion (approximately PLN 6.04 billion), an 11 per cent year-on-year increase.

This is the culmination of a long-term trend – in just five years, the sector’s total revenues have increased by an incredible 250%.

This trajectory was not without its challenges. There was an 8 per cent decline in 2021, but this was a predictable correction after an unprecedented digital entertainment boom in pandemic 2020.

The ability to return to growth quickly in 2022 proves that the market’s foundations are sound and its development stable. Nevertheless, in terms of total revenue, Poland is still behind Europe’s largest markets such as the UK, France, Germany and the Nordic countries, which is an interesting paradox in the context of the size of the workforce.

Global reach: an export phenomenon

At the heart of the Polish games sector is its almost complete orientation towards foreign markets. As much as 96-97% of revenue comes from exports, making games one of Poland’s most successful cultural and economic products on the international stage.

The geographical structure of these exports is diversified and demonstrates strategic maturity. Sales are evenly distributed across three key regions: North America, Europe and Asia, which together account for 75% to 90% of total sales.

North America, with the US in the lead, remains the most important single market.

Europe (UK, Germany, France) is the second pillar of sales.

Asia (China, Japan, South Korea) is the third prospective area of expansion.

Importantly, Polish studios not only create games, but also understand global markets. Polish horror movies are successful in Japan, while strategy games and simulators are hugely popular in Germany and South Korea.

The technological underpinning of this reach is digital distribution, accounting for more than 85% of sales and allowing even small studios to compete on the global stage.

Driving force: the fastest-growing talent centre in Europe

Behind the financial performance is the most important resource – human capital. In 2023, the sector will employ more than 15,200 people in some 494 studios, placing Poland among the top three largest gamedev labour markets in Europe, alongside the UK and France. What’s more, the employment growth rate is estimated to be the fastest on the continent.

At the same time, the ecosystem is extremely diverse. Alongside giants like CD Projekt RED, its strength is the dense network of smaller players – as many as 78% of the studios are teams of less than 25 employees, which is a forge for innovation and human resources.

The workforce is also becoming increasingly international and diverse: 24-25% are women (one of the highest rates in the world) and more than 14.5% are foreigners, mainly from Ukraine.

However, the picture of the ’employee market’ is not without its shadows. The industry is still struggling with the phenomenon of ‘crunch’ – periods of intense overtime work. Although 81% of companies officially condemn it, as many as 27% of employees have experienced it in 2023, with a worrying 70% admitting to working excessive hours.

This discrepancy between declarations and reality points to deep-rooted cultural challenges that a mature industry must address.

The price of talent: salaries in Polish gamedev

The high demand for specialists translates into salaries well above the national average. In May 2024, the median gross earnings in the industry were around PLN 12 000, while the national average oscillated around PLN 8 000. However, earnings are highly variable.

An analysis of the median total cost to the employer shows that the highest paid are production specialists (PLN 15,000) and programming specialists (PLN 13,900), with design (PLN 10,500) and graphic designers (PLN 10,300) in the middle of the pack.

The key drivers of salaries are location and company size. Warsaw is the salary capital, with the median over 20% higher than in the rest of the country. Employees at the largest studios earn on average more than 45% more than their colleagues in small teams.

The gender pay gap remains a complex issue. The median for men is PLN 12,000 and for women PLN 10,000. Surprisingly, the largest gap, 27 per cent, is in the graphics department – the same department that is the most feminised.

This suggests the existence of more complex, systemic barriers that go beyond the mere representation of women in teams.

Stock exchange: financial leaders

The maturity of the Polish games sector is reflected by its strong presence on the Warsaw Stock Exchange. An analysis of three key companies reveals the strategic diversity of the ecosystem.

- CD Projekt: Global flagship and titan of the AAA segment. Focuses on games with huge budgets, such as The Witcher and Cyberpunk. In 2024, the Group will reach PLN 985 million in revenue and PLN 470 million in net profit, with a market capitalisation of around PLN 26 billion.

- 11 bit studios: An innovator in the AA segment, creating games with a deep message (This War of Mine, Frostpunk) that ensure a long sales cycle. In 2024, the company recorded PLN 140.5m in revenue and PLN 6.9m in net profit, with a capitalisation of around PLN 445m.

- PlayWay: Unique business model, operating like an incubator. Diversifies risk by funding dozens of low-budget games per year, hoping for a few viral hits (Car Mechanic Simulator, House Flipper). This model brought in PLN 302.9m in revenue and as much as PLN 206.6m in net profit in 2024, with a capitalisation of around PLN 1.76bn.

The success of such strategically different companies is the strongest evidence of the maturity and resilience of the Polish games market.

The Polish games industry has entered a phase of maturity as a global player. Spectacular growth, export dominance, status as a European talent centre and strategic diversity on the WSE are the pillars of its strength. However, maintaining this position will require facing new challenges.

The global games market, soon to exceed $200 billion, presents huge opportunities. At the same time, there are challenges on the horizon: global consolidation and the risk of loss of independence , growing pressure from the capital market to deliver profits on a regular basis, the need to continuously feed the market with new talent through the education system, and paying off the ‘cultural debt’ – eliminating the crunch and closing the wage gap.

The next chapter in the history of Polish gamedev will be defined by how the industry copes with the complexities of global leadership. The challenge will no longer be just to make great games, but to sustainably scale the business and build a sustainable, ethical work culture.

This will determine whether Poland will consolidate its position not only as a manufacturing powerhouse, but also as a sustainable and influential centre of global digital culture.