For almost two decades, the Polish technology market acted as a ‘Swedish table’ in the global food chain. Foreign funds and corporations came to the Vistula to buy great quality code and competent teams at a reasonable price. However, the latest report M&A IT Industry 2025‘, prepared by Fordata and CMT Advisory, sheds new light on this landscape. The year 2025 is not a year of selling out. It is a year in which Polish technology companies have ceased to be mere prey and have gone on the hunt themselves.

Reversing the vector. Who deals the cards now?

Only a few years ago, the headline “Polish IT company acquires…” was a rarity, giving way to news of successive founder exits. The 2025 figures show a fundamental change in mentality and capital. Although Q3 2025 brought a market slowdown (a drop in the number of transactions of around 10% year-on-year), the structure of buyers is evolving.

As CMT Advisory and Fordata experts point out, home-grown players are increasingly bold in their role as consolidators. This is no longer just the domain of giants such as InPost (which continues to expand abroad, e.g. by acquiring Spanish Sending) or Benefit Systems. Medium-sized software houses and IT service providers that raised capital during the boom years (2020-2022) are entering the game. They are taking advantage of the current correction in valuations to build equity groups capable of competing in tenders in the US or Western Europe.

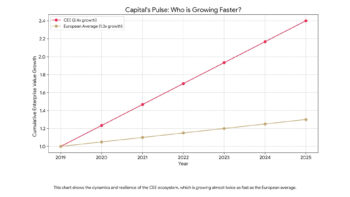

The Polish IT industry, which is responsible (together with the media and telecommunications sectors) for more than 20% of all M&A transactions in Poland, is becoming a regional centre of gravity.

Consolidation, or running to the front

Why are Polish entrepreneurs buying? The report suggests that the time of easy organic growth is over. Customer acquisition costs (CAC) and wage pressures have made it more profitable to ‘buy’ revenues than to build them laboriously from scratch.

In 2025, we see a clear trend:

- Acqui-hiring: acquisition of smaller entities mainly for development teams.

- Competency buying: Software houses buy boutiques specialising in AI or CyberSec to complement their offerings (cross-selling).

- Founders’ exits: as many as 71% of the sellers are private investors. This signals that the generation of founders who built companies in the last decade is looking for stronger capital partners – often precisely the larger, Polish players who understand the local specifics better than a fund from London.

What are we buying? TMT and “Smart Money”

However, not everything finds a buyer. A report by Fordata and CMT Advisory clearly indicates that 2025 is the year of selection. Investors, armed with professional analytical tools and a Virtual Data Room (VDR), are conducting much deeper due diligence than in the boom years.

Primarily product (SaaS) companies and those that are realistically implementing artificial intelligence – not as a marketing slogan, but as a scalable part of the business – are on target. An example that electrified the market in 2025 was the sale of IAI Group (an e-commerce platform) by MCI Capital. Although the buyer here was a foreign fund (Montagu PE), the transaction demonstrated that Polish SaaS products are achieving global valuations and that Polish funds (like MCI) are capable of making spectacular divestments, freeing up capital for further investments.

Is this the end of foreign capital?

Absolutely not. Foreign has not disappeared, but it has changed its strategy. PE/VC funds, which accounted for less than 10% of purchases in Q3 2025, have become more picky. They are looking for “diamonds” – companies with an established track record and recurring revenue (ARR).

For Polish companies, this is good news. The strong presence of local buyers creates a ‘safety cushion’ and sustains valuations, providing an alternative to exit. If you are not bought by an American strategist, a Polish competitor who is currently building a regional champion may do so.

Maturity has its price

The M&A 2025 report dispels the myth of a crisis in the IT industry. We are experiencing normalisation and professionalisation. The lower number of transactions in some quarters does not mean stagnation, but that the market has become more demanding.

For Polish CEOs and founders, the conclusions of Fordat’s and CMT’s analysis are clear: the era of being ‘Europe’s cheap labour’ is over. The era of building value through acquisitions has begun. The question for 2026 is no longer “who will buy us?”, but “who will we acquire to grow faster?”.